DeFi is the New Fintech

Decentralized finance disrupts the supply and distribution of money, enabling it to do what fintech fundamentally can’t

Decentralized finance disrupts the supply and distribution of money, enabling it to do what fintech fundamentally can’t

Decentralized finance — or DeFi for short — is an umbrella term for financial products built on top of open-source blockchains. DeFi is about creating an ecosystem of open finance accessible to anyone with a smartphone and an internet connection.

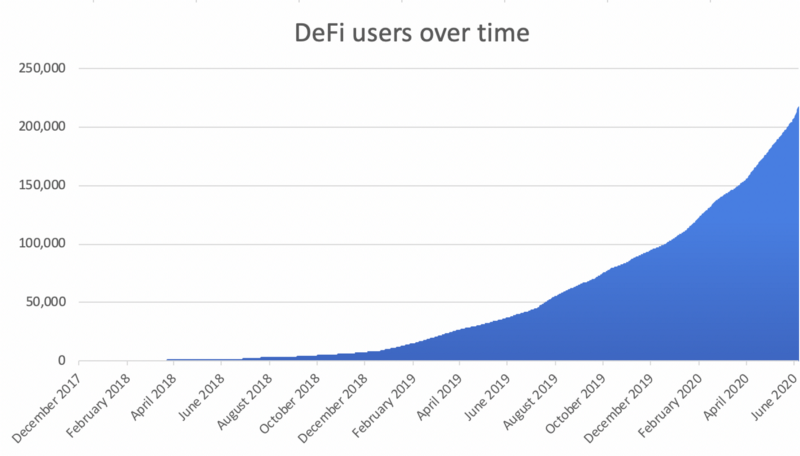

The DeFi ecosystem has seen massive growth over the past year, with the majority of DeFi assets having only been created in the last 6 months.

In this article, I’ll revisit what makes DeFi so unique and why it’s positioned to achieve what fintech fundamentally can’t.

Where fintech failed

Access has been at the heart of fintech for a long time. Unfortunately, the “fintech revolution” has fallen short on many of its aims because it’s essentially a modified UI to the same operating system. Companies like PayPal, Stripe, Robinhood and Transferwise have certainly made it easier to make online payments, invest in stocks, or transfer money across borders — but they don’t change how financial institutions work. The hierarchies, barriers and constraints are still there.

The same could be said of mobile money in places like East Africa, where telecom companies have made it easier for people to access mobile banking, but haven’t addressed structural issues around the capacity to leverage those services. A 2020 survey of two of Kenya’s most populous slum communities found that 35% of individuals who used M-pesa had a credit limit equal to zero, while the mean credit limit was just 0.04 USD.

Fintech giants like PayPal are still inaccessible to entire populations. Nigerians are not allowed to make or receive payments on the platform despite the country having the largest economy in Africa and ranking 6th worldwide for number of internet users.

Where did fintech go wrong?

In the US, fintech adoption sits at only 46%, far behind countries like India and China, at 64% and 90% respectively. While we can’t dismiss the strides that fintech has made in making certain financial tools easier to use, it is clear that the industry remains heavily constrained. This is largely because fintech has been unable to disrupt the supply and distribution of money

This is where Aggregation Theory is a useful framework, as it explains why DeFi will do to money what fintech fundamentally can’t.

The “internet” of money

The way decentralized finance is built achieves two things: a) it decreases the distribution cost of financial instruments and b) it removes barriers to entry for all financial services.

Think about how the internet has disrupted just about every industry:

- Music: buying albums vs. using apps like Spotify and SoundCloud

- Retail shopping: walking into physical stores vs. Amazon, eBay and Shopify

- Learning: who needs a university education when there’s Coursera, Udemy and edX?

The driving force behind these disruptions is that a new technology dramatically decreased the distribution cost of a core product, creating a wave of new supply. The core business challenge shifted from how to get the product to the consumer to how to compete for a consumer’s limited attention on aggregator platforms.

We’re seeing a similar trend in finance, where the supply and distribution of financial services (and sometimes even money itself) has become modularized. Anyone can create money or a new financial product with almost zero costs — think of how Curve was created by a one-man team and has already processed over $200 million within 4 months.

Consumers have no problem accessing these new products because everything is digital — in most cases all they need is an Ethereum wallet. The burden is now on the creators of these products to compete for consumer use, as seen in trade volumes and market capitalizations. The financial landscape is inching closer and closer to what the economist Friedrich Hayek wrote about in his 1976 book, The Denationalization of Money: we’re entering an era of privately issued, competing fiat currencies.

Unfortunately, fintech has been unable to modularize the supply and distribution of its core product. Traditional finance remains extremely localized, distribution costs are enormous, and the scale and pace of innovation are impeded because there is an entrenched monopoly over who gets to create financial products.

Below I look at how DeFi takes a fundamentally different approach to addressing these challenges.

What makes DeFi so unique?

DeFi is programmable and acts like a universal settlement layer. The Ethereum Virtual Machine removes the need for third parties to facilitate transactions such as the legal system, banks, brokers, auditors, exchanges, etc. Within centralized finance, each middleman contributes to the final cost and duration of contract execution, driving up costs and creating barriers at every turn. However, with DeFi you can look at the code of a contract and be sure it will be executed as written. Because functions are controlled by smart contracts and not people, transactions happen within seconds and costs are significantly lower. In theory, dapps (decentralized apps) can run themselves with virtually no human intervention.

DeFi is transparent and permissionless. There are no gatekeepers restricting who can create and participate in DeFi services. It’s incredibly easy to bootstrap DeFi projects with just a small team and virtually no funding. For example, 1inch.exchange was built by a two-man team at a hackathon in New York in 2019, and has already processed more than $500 million. Anyone can access the code to a smart contract in order to understand how it functions or search for bugs, and all transaction activity is publicly viewable on sites like etherscan.io.

DeFi is borderless and non-custodial. Smart contract executions cannot be meddled with by users, therefore DeFi has no need for checks and balances to mitigate counter-party risk. This is why most dapps don’t have KYC (Know Your Customer) processes and are immediately accessible to anyone with an internet connection, a smart phone, and an Ethereum wallet. Because there are no middle men, users have the choice to remain the sole custodians of their assets at all times.

DeFi is interoperable. Different applications can be built on top of each other and customized in new ways, regardless of who created them. The entire system is a bit like a box of Lego blocks — there is no limit to what can be built. Because smart contracts serve as a common settlement layer, DeFi products can be accessed through any platform that supports Web3 integrations. This explains why there has been such a proliferation of DeFi interfaces like Zerion. The platforms that survive are the ones that provide the most benefit to users, so this competition improves the quality of the entire ecosystem.

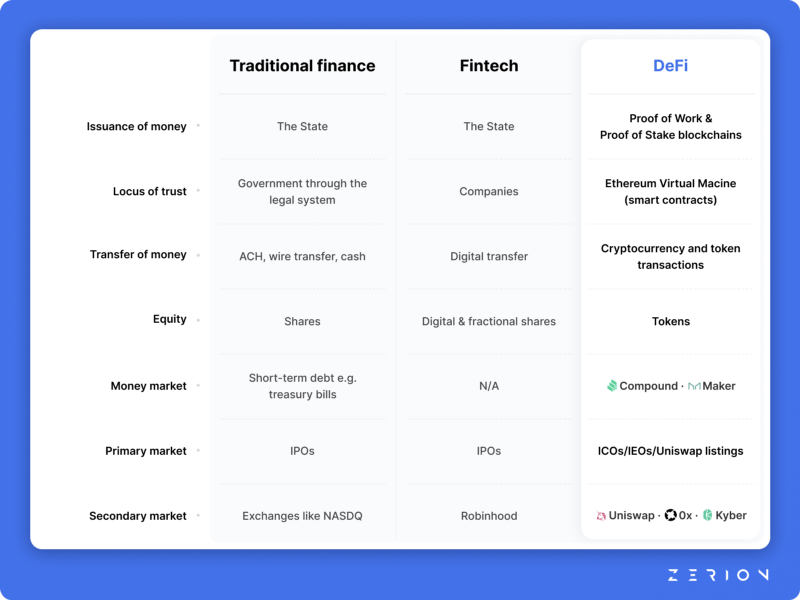

The table below summarizes how DeFi differs from traditional finance and fintech:

Scaling DeFi

DeFi’s unique infrastructure explains why there is such rapid growth in the space. For example, over 100 DeFi projects were created at the HackMoney Hackathon and VC investment has channelled over $86 million into DeFi between 2019 and 2020.

The next challenge will be to make these new financial instruments more accessible to a broader audience. The burden on designers and developers is to remove the friction between highly sophisticated financial tools and users looking for ease and simplicity. If the current pace of innovation is anything to go by, we’re not far off.

Catch my full presentation at CogX 2020: “DeFi is the new fintech”: