The Missing Layer in Stablecoin Infra: Wallet Data

Stablecoins are in production. But wallet data is still built in-house. Learn why the blockchain data layer is the next fintech infrastructure shift and how to skip the build.

Stablecoins are no longer a question. They are now in production at banks, payment networks, and fintechs: accepting payments, holding treasury, paying out to customers and contractors. The liquidity is there. The regulatory clarity is there. Most of the infrastructure is in place.

The hard part of stablecoins has moved underneath. The infrastructure for issuing, custodying, and routing stablecoins is increasingly off-the-shelf. Yet the infrastructure for reading stablecoin balances and transactions is mostly still built in-house. That's the wallet data layer, and it has hidden costs.

The hidden tax of blockchain data

Every fintech that adds stablecoin support inherits a multi-chain data problem it didn't sign up to solve.

There are now more than 200 stablecoins in circulation across over 37 blockchains. The "same" stablecoin on Ethereum is not the same as it is on Solana. It has different supply, different liquidity, and different technical standards. Yet customer balances and operations all need to happen across all blockchains consistently.

Most teams handle this with internal engineering.

Each new supported chain adds another integration, another set of edge cases, another team meeting about why a balance didn't show up on time. The cost compounds quietly: missed transactions during reconciliation, gaps during audits, support tickets, throughput failures during volume spikes.

Running production stablecoin operations becomes a continuous engineering expense.

But this operation doesn't differentiate your product for your customers. This blockchain wallet data is something that can be delegated.

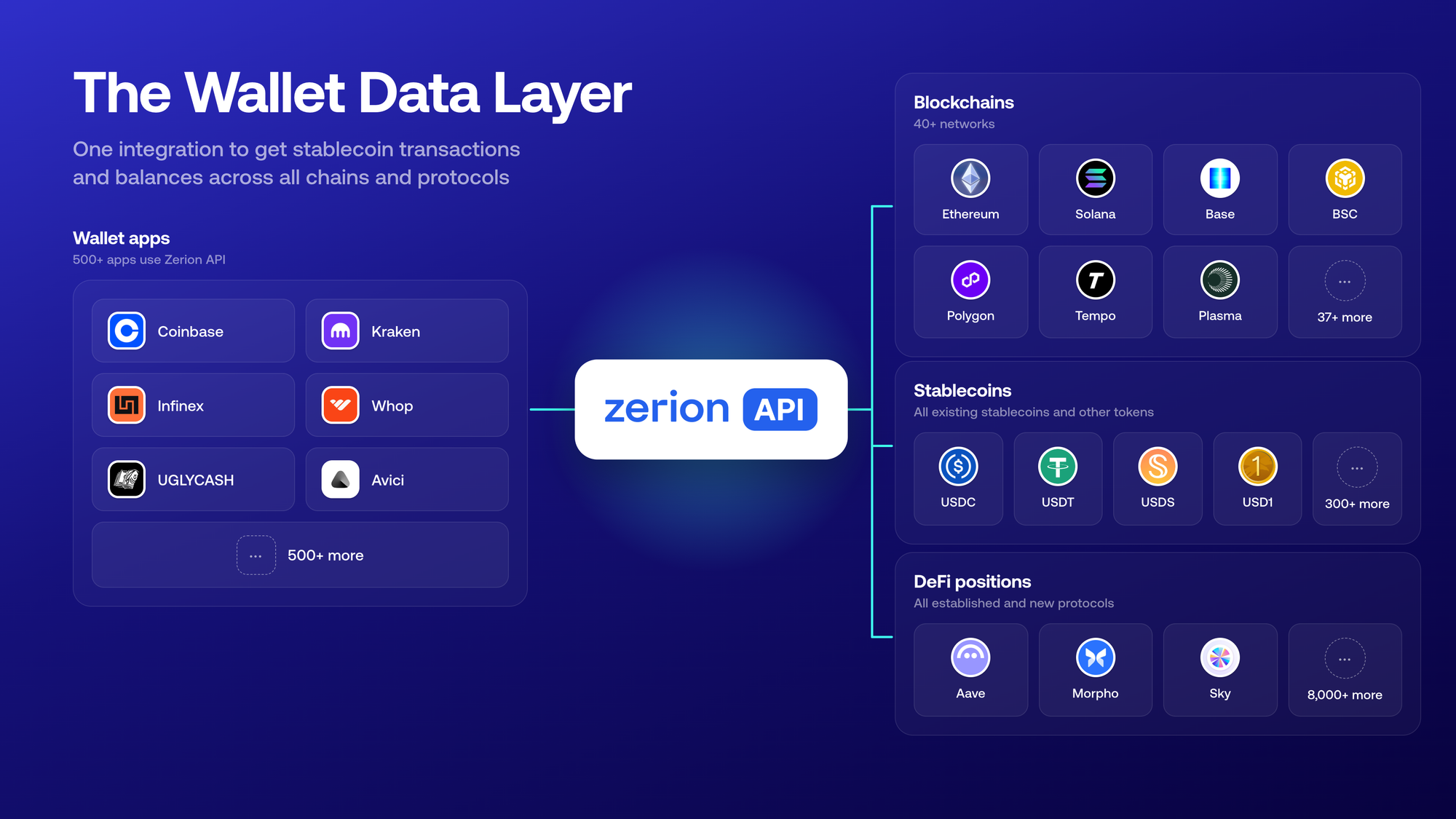

What a wallet data layer does

Blockchain data is public. Yet turning data into information that customers expect isn’t trivial.

A wallet data layer like Zerion API turns raw onchain activity (token balances and transactions) into clean, consistent information your product can use.

It replaces a chain-by-chain build with a single integration. It normalizes data across ecosystems. And it does this with the throughput, uptime, and scale of an enterprise.

A single call to a wallet data API returns one clean answer. Producing that answer in-house means a team has to take ownership of five ongoing responsibilities on every supported blockchain:

- Run the infrastructure. Operate blockchain nodes to get the block data, reliably and around the clock, with capacity for traffic spikes.

- Track every address. Process every new block as it arrives, identifying which transactions affect which customers.

- Interpret and label activity. A transaction's raw record shows that something happened, not what it means for user holdings.

- Maintain a searchable history. Keep the result in a database that your product teams can query with the responsiveness an enterprise expects.

- Keep it accurate over time. Handle the long tail of edge cases that pile up as chains evolve, smart contracts get added, and customer behavior changes.

Each of these is a real engineering discipline. Building them is possible. It just isn't something your customers pay you for.

Fintech has been here before

This pattern isn't new.

Just over a decade ago, every fintech that wanted to read a customer's bank balance had to build it themselves. Connecting to a single bank was hard. Connecting to every bank a customer might use was a project that ate engineering teams alive.

Companies like Plaid and Yodlee turned bank connectivity into infrastructure.

Plaid was founded in 2013. Its first major customer was Venmo, which needed a reliable way to verify customer bank accounts. The pattern caught on quickly. Today, Plaid powers apps for 12,000 financial institutions with over 100 million customers in total.

Plaid and Yodlee didn't win because they built bank connectivity better than the fintechs that hired them. They won because the rest of fintech decided not to build it at all.

Similar trends happened in other parts of the fintech stack: KYC, card processing, payments, and others.

The companies moving quickly on stablecoins today are making the same decision about onchain data. Treat it as plumbing. Focus on the product your customers pay for.

The opportunity on the other side

When the blockchain wallet data layer stops being a build problem, the roadmap conversation changes.

Product teams stop asking "can we even read this chain?" and start asking "what should we build for customers next?" Treasury teams start running stablecoin operations like bank accounts. Compliance departments stop assembling audit trails by hand.

Successful fintech apps didn’t try to reinvent card processing, bank aggregation, and KYC infrastructure. Instead, they treated them as infrastructure and focused on the products on top.

Stablecoin wallet data is the next layer.

The adoption is already there. The only question is how to read this data at scale.

Zerion API is the wallet data layer behind 2,000 apps, including some of the largest names in crypto, fintech, and payments. If you're building anything that touches stablecoins, reach out to our team by sending an email to api @ zerion.io. Or check the docs and sign up to get a free API key.